Bill Quickel's - Insurance Plus Agencies Inc. Blog |

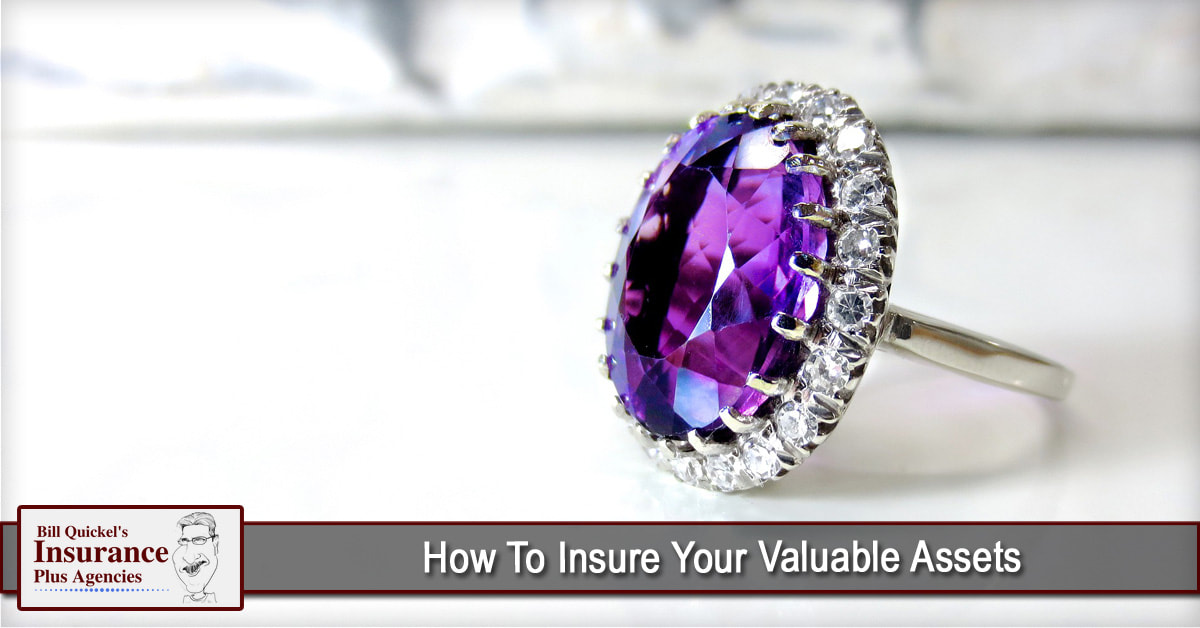

The insurance policy that covers damage to your television may fall short when it comes to an inherited diamond necklace. It's one thing to insure the Chevy you drive to work every day, but quite another to cover loss or damage to a rare, 1940s-era Rolls Royce, an antique watch or a Jackson Pollock painting. Your traditional homeowner's insurance policy rider may fall short, requiring the purchase of a more sophisticated policy.

Jim Fiske, a vice president at Chubb Personal Insurance in Warren, N.J., says people should look at their collectible items both quantitatively and qualitatively when determining whether specialty coverage is needed. "Anything with value that goes beyond your traditional policy -- or if something presses a button for you emotionally so that you'd feel a personal loss, whether it be cars, wine or jewelry," probably requires specialty coverage, he says. Specialty insurance also comes with a variety of services not found in typical policies, such as referrals to qualified shipping companies if a painting is being transported overseas for display, as well as coverage for the work of art during shipping and exhibition, Fiske says. Other services include storage facility inspection and referrals to appraisers and restoration experts. The cost of coverage will vary depending on the item and its intended use. For example, an antique car that is driven to exhibitions has a higher risk of damage and will cost more to cover than one that sits in a museum. Jewelry is a little more expensive to insure than a painting, Fiske says, because it's being worn, while a painting typically remains in a static location. But the rule of thumb is that the annual premium for jewelry will be about 1 percent to 2 percent for every $100 of the item's worth; fine art will be less than a half a percent for every $100 of its value and collectible cars will be higher than either of those, depending on mileage limits. When evaluating specialty insurance companies, Fiske says, look for experience as well as expertise in the assets you want to insure. Find out what the process is like if you have to make a claim, he adds. "Does the company have an 'in' with specialists who can repair or replace the lost or damaged items?" Although theft is the top concern for most policyholders, Fiske says that's not as common as you might think. "I find people tend to spend a little too much time worrying about the movie 'Gone in 60 Seconds,' or a Cary Grant-type cat burglar," he says, "but the real threat to any collection isn't movie-plot thefts, it's the facility itself and damage from fires, earthquakes, hurricanes and those types of catastrophes." Judy Martel - Judy Martel, CFP, is a writer and editor. She blogs about wealth on Bankrate.com and is the author of "The Dilemmas of Family Wealth," published by Bloomberg. See us for more details on your "Treasures" 740-992-6677 or www.114court.com Also look at our Allstate Site The New Improved Allstate Digital Locker for a free home inventory. Look for the Digital Locker phone toward the bottom.

4 Comments

8/26/2021 09:33:22 am

If you want to protect your valuable assets like jewellery and money, save them in safe which is protected by high-tech locks. 9/15/2021 06:13:27 am

If you want to secure your valuable assets, secure them in safes which is secured by strong combinations. 10/8/2021 11:52:27 am

The password secured safe are best to keep your valuable asset secure from thieves. 7/8/2023 07:27:41 am

says people should look at their collectible items both quantitatively and qualitatively when determining whether specialty coverage is needed Leave a Reply. |

Contact Us(740) 992-6677 Categories

All

Archives

January 2020

|

RSS Feed

RSS Feed