Bill Quickel's - Insurance Plus Agencies Inc. Blog |

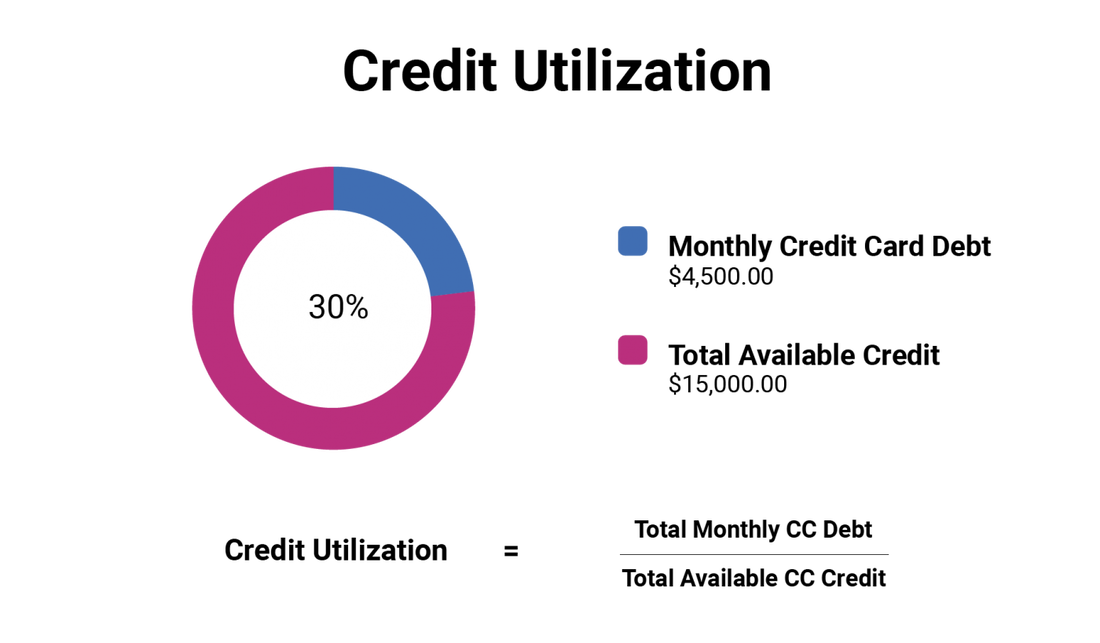

There is a common misconception that carrying a balance on your credit card from month to month can benefit your credit scores, but that is not true. Ideally, you should pay off your credit card in full every month. Carrying a balance will not help your credit scores. All it will do is cost you money in the form of interest, and probably hurt your scores in the process. Factors That Influence Your Credit Scores The most important factor in credit scoring is always your payment history: whether or not you make all your payments on time. The second most important factor is your utilization rate, or balance-to-limit ratio. To calculate it, add up the monthly statement balances on all your credit cards and divide into the total credit limit across all your credit cards. For example, say you have three credit cards, each with a credit limit of $5,000. Thus, your total credit limit is $15,000. If you spend $1,500 on each card each month, your total monthly utilization is $4,500. Divide that by your credit limit of $15,000, and you get a credit utilization ratio of .30, multiplied by 100 to get 30%.  The lower your utilization ratio, the better it is for your credit scores. It's Best to Pay Your Credit Card Balance in Full Each Month If you are trying to establish a strong payment history, you can do so by making small purchases on your credit card each month, paying the balance in full, and making sure all payments are made on time. If you cannot pay the balance in full, keep the balance as low as possible. You should never carry a balance of more than 30% of your credit limit on any one card or in total. The lower your balances, the better it will be for your credit scores. Making small purchases and then paying them off right away will keep the card active and keep your balance well below your credit limit. This demonstrates that you consistently manage debt well and can help increase your credit scores. Paying Your Credit Card Bill Before the Statement Generates Paying your balance off in full each month does not negate the impact of utilization. The utilization ratio is calculated by dividing your monthly statement balance—the amount that is shown on your bill—by your borrowing limit. So if you have a $10,000 credit limit and spend $2,000 on your credit cards each month, you will show a 20% utilization ratio even if you pay off those charges in full every month. You can, however, be strategic about lowering your utilization ratio if you pay off your bill early before your statement generates. So if you have a total credit limit of $10,000, spend $4,000 on your credit card, but pay off $3,000 of that spending before your credit card statement generates, your statement will only reflect $1,000. Thus, your utilization ratio will be considered 10%, not 40%. Blog Post by: Ismat Mangla

2 Comments

7/8/2023 07:55:54 am

Carrying a balance will not help your credit scores. Leave a Reply. |

Contact Us(740) 992-6677 Categories

All

Archives

January 2020

|

RSS Feed

RSS Feed